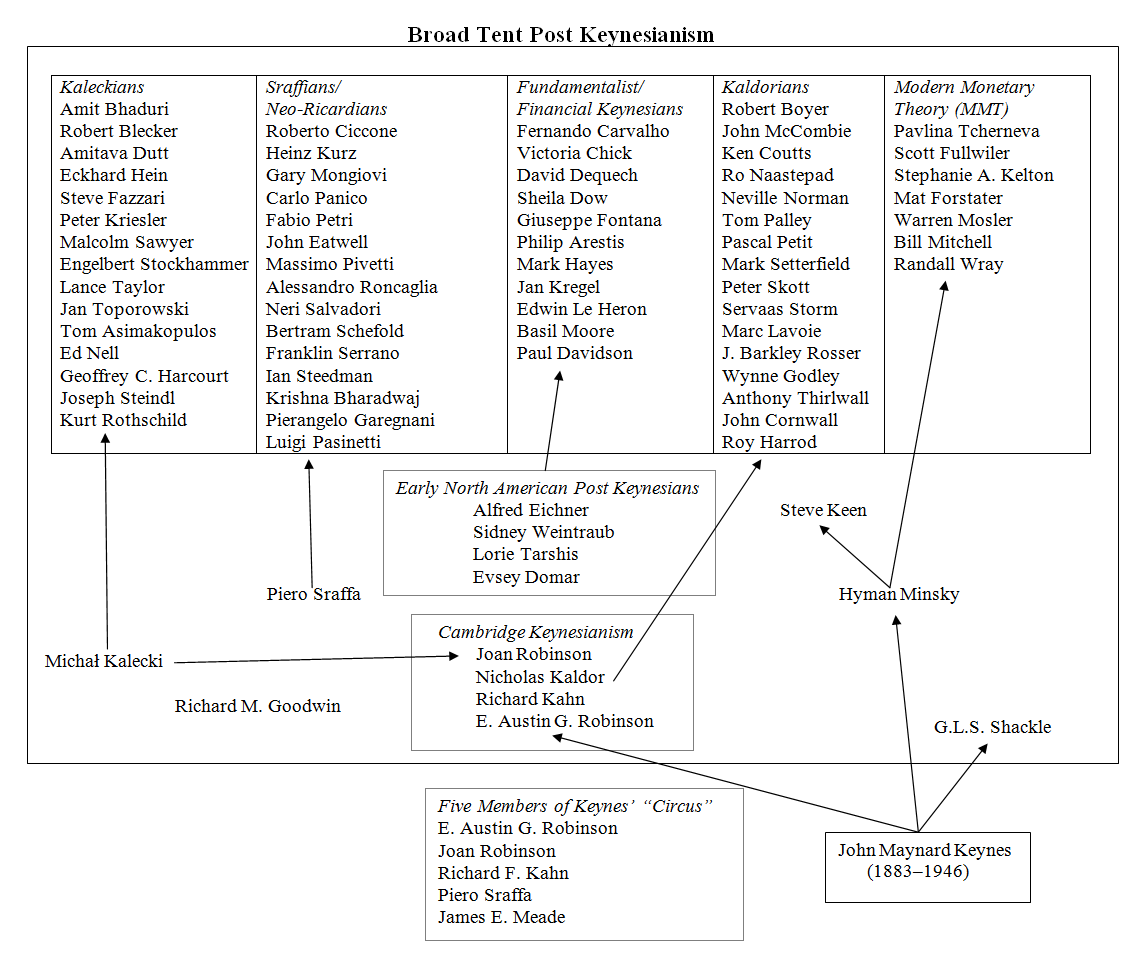

I believe the very first comment I got on this blog was from someone who said I should check out Post-Keynesianism. At the time, I only had a vague understanding of what it was. It seemed to me to be an odd name for something that appears to flow from contemporaries of Keynes (Robinson, Kalecki, Kaldor all get mentions).

Now, after ten years of hanging out in the econoblogosphere, I still have no idea what Post Keynesianism is. When Noah Smith posted his rant the other day that seem specifically directed at Post Keynesianism, it came to my attention that many of the people I follow on Twitter or in blogs range from sympathetic to enthusiastic toward Post Keynesian economics. As I hope not to alienate too many people, let me start with some positives ...

Inasmuch as Post Keynesianism flows from Keynes' General Theory, Post Keynesianism will generally be more consistent with the present state of many major economies: US, EU, Japan. The IS-LM model is an (effective) theory of low inflation. Austerity during a demand slump is generally bad; government spending is not always bad (and has many good uses). Monetary policy is sometimes an ineffective tool of demand management.

Post Keynesians are critical of mainstream economic methodology and seem to take a pluralistic approach. This is as it should be because there seem to be few empirical successes coming from mainstream economic methodology.

(+) Joan Robinson won the Cambridge capital controversy

I managed to show this with a bit of group theory and information equilibrium -- you might find it entertaining.

...

Noah followed up with a Tweetstorm that really helped me understand what Post Keynesianism is -- it is basically activism in the mold of the "Chicago school", but from the left (so I am sympathetic). It starts with conclusions (either free markets or government intervention) and accepts 'methodologies' that yield them. In contrast to the Chicago school, Post Keynesianism has found a pluralistic confederation of methodologies. Now since a) non-zero government intervention is generally a good thing (most advanced economies have evolved into mixed economies) and b) they derive from Keynes' General Theory, many of the Post Keynesian methodologies will yield correct results. Paul Krugman is generally right about everything and uses IS-LM to explain his thinking on his blog.

(You probably knew that was coming ...)

(–) Many of the Post Keynesian methodologies (also) fail to be frameworks

Kaldor-esque non-linearity is not a framework. Newtonian systems can be non-linear; so can biological systems. These are not the same framework, so non-linearity does not define a framework. Kaleckian Post-Keynesian economics defines a business cycle to depend on investment; Minsky-based approaches to the business cycle assume a business cycle is credit and optimism -- neither create tools for research to discover what a business cycle is. You can't define the business cycle -- one of the main phenomenon of macroeconomics -- with your framework.

It's apparently acceptable in economics to define the phenomenon you want to understand with your framework. One way to understand what a framework is is to ask whether the world could behave in a different way in your framework ... Can you build market monetarist model in your framework? It doesn't have to be empirically accurate (the IT framework version is terrible), but you should be able to at least formulate it. If the answer is no, then you don't have a framework -- you have a set of priors.

Most of mainstream economics also fails to have a framework. That's because frameworks generally organize empirical successes -- and as I said above, there aren't a lot of those. Speaking of empirical success ...

Showing the direction and/or relative magnitudes of effects is a start, but it's not an empirical test. Additionally, many of the stock-flow models have a ridiculous number of parameters. That makes them just as inconclusive as mainstream DSGE models. Speaking of which ...

I didn't discuss this in the methodologies section because this is (kind of) a framework. But it's a limited one. I wrote about this before here, but I wanted to say more.

E² = p² + m²

that's stock² = flow² + stock².

Or this standard damped oscillator:

ẍ + (1/τ) ẋ + ω² x = 0

that's change in flow + flow + stock = 0.

In the information equilibrium description of a transistor, I take a derivative of a stock with respect to a flow (dV/di). Ever thought of taking a derivative of investment with respect to money?

The thing is when you directly relate stocks with flows, or in general mix up the units together, science happens. Important scientific constants have mixed up units, h-bar is [J-s], c is [m/s]. Mass is basically the constant of proportionality between force and acceleration. Electrical resistance R converts electrical flows (current) into electrical stocks (voltage) (stock = flow * R).

Stock flow analysis is basically analogous to Kirchhoff's laws: detailed accounting of stocks (voltages) and flows (currents). The various things (households, central banks, government) are the various circuit components (inductors, resistors, batteries). But the dynamic behavior of an RLC circuit comes from the behavior of the components, not their contribution to the balances in Kirchhoff's laws. Those balances just couple them together, but the physics is in how the components behave. In those stock flow analysis tables (e.g. see below from Lavoie-Godley [pdf]), the economics is in how the various nodes behave. This behavior is usually implicitly included in the specific choice of the relative time indices and the linear relationships (and which things to include) ... and some handwaving assures us this is just "accounting".

|

| Stock-flow analysis from Lavoie-Godley [pdf] |

Y = C + I + G + NX

There are several different models you can make from this accounting identity alone -- including both IS-LM and Nick Rowe's market monetarist model. I discuss this more extensively here.

(–) Accounting may not be terribly useful for economics

I think I know what's going through your head right now -- What??!

Lots of different models can be consistent with any given accounting identity. So tell me what the other stuff is that makes your model your model -- I don't care about the identity. Lots of different circuits can be built with the same circuit components that all maintain Kirchhoff's laws (accounting identities for electric charge). This is why I prefer information equilibrium relationships -- they tell you what's in the model.

But also: accounting approaches effectively mean the whole is (in some way) the sum of its parts. This is not true for companies (made up of dark matter) and may not be true of the economy in general. For example, it isn't true in the IE model. The macro accounting identity contains an "entropy" term that only exists because there are multiple markets.

And then there are things like the intertemporal budget constraint -- something that should (at best) hold approximately, and generally not during a recession. Any time you relate one time period to another with accounting, you are using an intertemporal accounting identity.

Anyway, my Post Keynesian readers probably hate me now. But I encourage them all to jump in on the wave of the future! Information transfer models!

You can probably build many of the Post Keynesian models as IT models anyway. Start with the IS-LM model. The IT IS-LM model is actually empirically accurate (good to leading order, anyway):

For what it's worth, I have stronger opinions about market monetarism.

This comment has been removed by the author.

ReplyDeletetl;dr version: I used to be a PK "fan" but can't claim to have ever understood it that well. Great post!

ReplyDelete"The IT IS-LM model"

ReplyDeleteLS-MIIT? ;)

Or has nobody heard of that these days?

Huh?

DeleteAs I thought.

DeleteLS-MFT. Lucky Strike Means Fine Tobacco.

One thing that has amazed me is the apparent animosity of some economists to identities. Despite the fact that arguments by economists (at least in blogs if not academic papers) often enough fail to take them into account. When that fact is pointed out, the usual response is, Oh, that's an identity, of course we all know that.

ReplyDeleteSometimes I wonder if those economists are like people who learned the principle of minimum action and therefore disparage the conservation of momentum.

A conservation law is not the same thing as an identity.

DeleteI could freely declare A ≡ B + C or A ≡ X + Y + Z. This doesn't mean that A is now "conserved".

Additionally, saying

Y = C + I + G + NX

is like a conservation law is the opposite of what Keynesian economics says (i.e. that it's not a conservation law ... adding G + dG gives you Y + dG, not Y = Y0 and e.g. C becomes C - dG).

Conservation of momentum is a result of spatial translation symmetry, and is not an identity. If you break spatial translation symmetry, you'd get non-conservation. It's true that this doesn't seem to be true of the real world, but the real world probably does break supersymmetry ... which is just an extension of the Poincare symmetry of which spatial translation symmetry is one component.

A conservation law is not the same thing as an identity, but it is an equation that always holds. Within the theory, it acts like an identity.

DeleteHence: "A body will remain in a state of rest or uniform motion, except inasmuch as it doesn't." -- Eddington ;)

Jason: "Additionally, saying

Y = C + I + G + NX

is like a conservation law"

I am saying that a conservation law is like an identity.

Jason: "is the opposite of what Keynesian economics says (i.e. that it's not a conservation law ... adding G + dG gives you Y + dG, not Y = Y0 and e.g. C becomes C - dG)."

Here is the kind of thing I am talking about. Economist says, "Increasing government spending will increase GDP by the same amount." You say, "What about dY ≣ dC + dI + dG + dNX?" Economist replies, "Everybody knows that." Or: Economist says, "Increasing government spending will decrease investment by the same amount." You say, "What about dY ≣ dC + dI + dG + dNX?" Economist replies, "Everybody knows that."

See your own "Beware Implicit Modeling" post. :)

Yes, excellent post! :)

ReplyDeleteYours was a gallant attempt, Jason, but-I'm sorry to say-it failed. It's not your fault: there isn't really a single post-Keynesianism in any significant way.

ReplyDeleteWhat there is is a confederation of people whose common denominator is opposition to "mainstream economics" (ME), many/most claiming to be the sole rightful heirs and interpreters of Keynes. That's not new. Check Amartya Sen's Biographical notes at the Nobel Prize website

http://www.nobelprize.org/nobel_prizes/economic-sciences/laureates/1998/sen-bio.html

Last January, considering that "it seems that each heterodox economist is a one-man church" Asad Zaman (from the Real-World Economics Review Blog) entitled a post with this question: "Is there a core of heterodox economics that we can all believe in?"

He found-surprise, surprise-that there isn't any (you can check a series of related posts, here: https://rwer.wordpress.com/)

What applies to heterodox economics, also applies to post Keynesianism. Because of that, post Keynesians are big on methodological critique; the problem is that they hardly agree on what is wrong with ME. Take their position regarding maths in economics: Tony Lawson (a big name), says that maths is the single biggest problem with ME; Steve Keen (another big name) thinks maths is the way to go (but ME uses the wrong kind of maths).

Because their focus is criticism, few have explicit theoretical proposals (as far as I can tell, Keen and MMT are the ones with something more or less concrete, although in Keen's case I'm rather sceptical).

Policy-wise they tend to favour government intervention, within a capitalist system. As Sen writes: "In an obvious sense, the Keynesians were to the 'left' of the neo-classicists, but this was very much in the spirit of 'this far but no further'."

I suppose it depends on one's definition of Left. If that makes them lefty, then they do tend to be Left. In that, ironically, they may be to the left of Keynes. Some, however, are much less left; in fact, there is a kind of mutual sympathy among some Austrians and some post Keynesians.

Neither are they really for "pluralism", in general. Those who speak of pluralism often really demand that mainstreamers should be pluralistic towards their own "one-man church", and, once in positions of some authority, the calls for pluralism magically cease.

If one thinks about it, "pluralism" is a rather naive idea: one believes one's theory is right, therefore different theories must be wrong. What place can pluralism have?

AnonymousE

If one thinks about it, "pluralism" is a rather naive idea: one believes one's theory is right, therefore different theories must be wrong. What place can pluralism have?

DeleteThere could be a case made that if there is a single fundamental theory, there is one theory to rule them all.

But as I wrote -- and David Glasner re-posted -- even physics doesn't resort to a single theory to describe everything. The 'more fundamental' theories are in practice supplanted by effective theories at different scales.

Post Keynesian pluralism may partially represent that -- different theories for different problems.

...

But it is odd to start off saying I failed because Post Keynesianism is pluralistic, but then conclude that Post Keynesian pluralism is naive.

What could have been my aim that makes sense of that criticism?

Did I fail at taking down Post Keynesianism? That wasn't my aim -- I was offering a critique. There are pluses and minuses. And in that list, I called pluralism a plus. So I failed in taking down PK because it is pluralistic -- because I called pluralism a plus?

...

I do agree that my take on PK above isn't exhaustive. I picked a couple of things.

"Last January, considering that "it seems that each heterodox economist is a one-man church" Asad Zaman (from the Real-World Economics Review Blog) entitled a post with this question: "Is there a core of heterodox economics that we can all believe in?"

Delete"He found-surprise, surprise-that there isn't any"

I am reminded of the afternoon in high school when a friend of mine and I perused the long list of heresies in the Catholic Encyclopedia at the local library. So many heresies, One True Church. ;)

"He found-surprise, surprise-that there isn't any"

But it is odd to start off saying I failed because Post Keynesianism is pluralistic, but then conclude that Post Keynesian pluralism is naive.

ReplyDeleteI don't think I said Post Keynesianism is pluralistic. And I don't think I said your failure was in taking PK down, either. :-)

What I said is that PK "is a confederation of people whose common denominator is opposition to 'mainstream economics', many/most claiming to be the sole rightful heirs and interpreters of Keynes."

A dysfunctional family can unite against the neighbours; that doesn't mean Mom and Dad love each other or even get along.

Assuming you are the same anonymous as above, you did say it was pluralistic:

DeleteIt's not your fault: there isn't really a single post-Keynesianism in any significant way.

Not single PK = pluralism.

And you say:

And I don't think I said your failure was in taking PK down, either

I know you didn't say that ... the thing is that I had no idea what you meant, so I was suggesting a possible sensible thing that you could have meant. That's why I ended that sentence with a question mark.

"The IT IS-LM model is actually empirically accurate "

ReplyDeleteIt will be. The empirical data you are using has been created by policies conforming to the belief.

It is, in effect, a classic example of curve fitting.

You cannot empirically test your theories easy in the real world unless you restrict your theories to those movements a man can make in a strait jacket. Then you can prove them.

But you can't prove empirically what a man can do outside a straitjacket, because no such example exists in the real world at the present time.

So 'empirical testing' will just end up with something matching Paul Krugman and his IS-LM fetish - which even John Hicks rejected as a 'classroom gadget'.

People are not boron atoms or ants. They learn and adapt based upon feedback loops.

The empirical data you are using has been created by policies conforming to the belief.

DeleteI can assure you that the data was not created with the information equilibrium model in mind.

And if it is so obvious that models will fit data created to fit them, why don't any economists ever compare their models to data?

Economists explicitly say the IS-LM model is qualitative, not quantitative (Mankiw "Macroeconomics" 5th edition), so in general they won't make anything more than qualitative comparisons ...

like here

http://crei.cat/people/gali/jgqje92.pdf

Jason,

ReplyDeleteOK, so you've got attitude.

You are going to need more than that to swing opinion in your favour.

For starters, you have to get off your high horse and begin to explain concepts in a language that dumb bums like me understand.

Not everyone has a PhD in physics or maths.

Otherwise it's all looks like narcissistic grandstanding and you may as well forget it.

(Maybe I should have read Dale Carnegie thru a second time.)

Henry.

I thought you said math was "ineffectual" to understand economics ... you said:

DeleteMathematicians don't know how to model complex cyclical behaviour - even though their mathematical machines have the look of rigor, they are ineffectual. You can invent and invoke all the high sounding terms and concepts you like, the plain simple fact is that mathematicians don't understand cyclical behaviour.

If you don't think the math works, why should I explain the math in different language? It will mean the same thing.

If you think an explanation is "ineffectual" in Spanish, then it's not going to get any better in Italian.

None of the above is PhD level physics or math, either.

Jason,

Delete"I thought you said math was "ineffectual" to understand economics ... you said:"

Where have I said that? You always seem to be putting words into my mouth and misconstruing what I say. If I have said that somewhere, then I retract it. But I don't think I would have said exactly that. I would more likely have said economic insight does not require maths. Rigorous proof of economic relationships probably does. Maths should be the means to an end not an end in itself. It seems to me a great deal of academic theoretical economics these days is just mathematical narcissism and mathematical masturbation. There is a dearth of real economic insight. In some ways, maths can get in the way of real understanding.

"If you think an explanation is "ineffectual" in Spanish, then it's not going to get any better in Italian."

Bad analogy. Mathematics strictly can't be translated into another language. Mathematics is mathematics. Either you understand it or you don't. I studied physics and chemistry and high level maths at secondary school level and I have to say, I was pretty good at it. However, in my day, you had to study thermodynamics, quantum physics, differential equations (Lagrangians, Hamiltonians, optimization algorithms etc.) even matrices/linear algebra, at university level.

So if you want to pitch your model to dumb bums like me you will have to work harder and provide intuitive explanations. This will be a measure of your understanding of what you are offering.

If you want to pitch your work to academic economists you have a chance as most of them these days have studied maths at a sophisticated level and most of them are reworked physicists and mathematicians anyway.

You said it here:

Deletehttp://informationtransfereconomics.blogspot.com/2016/02/as-if-positive-economics-evolution-and.html?showComment=1455749562634#c7112168190368876332

But if you want to take it back, that is fine by me. It is definitely more productive to try and explain things to someone who doesn't assume what you are trying to say is bunk from the start.

:)

...

My analogy was that mathematics is another language. Anything that can be done with mathematics can be expressed in words -- we didn't grow up knowing math, so it had to be taught some way. And any mathematics can be expressed in words; e.g.:

dV/di = k V/i

"the rate of change of voltage with respect to current is proportional to the ratio of voltage to current"

There are no matrices, quantum physics, optimization algorithms, Lagrangians or Hamiltonians in the above post. There are only a couple of equations -- two of which reference calculus (derivatives).

I do mention entropy (thermodynamics), but I also say that the key point is just that something can be more than the sum of its parts:

But also: accounting approaches effectively mean the whole is (in some way) the sum of its parts. This is not true for companies (made up of dark matter) and may not be true of the economy in general. For example, it isn't true in the IE model. The macro accounting identity contains an "entropy" term that only exists because there are multiple markets.

You don't really have to understand what entropy is (it's actually an analogy itself) ... it's just saying in the information equilibrium model, the whole is more than the sum of its parts.

Jason,

DeleteI know where I made the extracted comments.

I am saying what I said is not the construction you have put on my comments. My comments were specifically directed towards cyclical behaviour not economics in general.

I think you are being a little bit cute in explaining about the way you explain your model, both verbally and mathematically. Your explications are not as simple and clearcut as you say. I have asked questions and the answers take me further down the rabbit hole. You direct me off to Wiki pages etc. which are bursting with novel (for me) complex concepts and mathematical explanations. If I had the time I would work thru them. I have enough trouble coming to grips with standard economics. My 40 year old degree in economics is a little dated.

Jason,

Delete"It is definitely more productive to try and explain things to someone who doesn't assume what you are trying to say is bunk from the start."

I don't think what you have on offer is bunk. I just don't understand it.

Some of your economic projections seem like statistical curve fitting and not related to your model. Nothing wrong with statistical curve fitting per se. It just seems that you're passing it off as IE model related. Probably got that all wrong. I'm sure you'll disabuse me of my error.

The forms of the equations that I fit to the data come from the IE model (specifically, solving the differential equation). The parameters aren't determined by the model -- that comes from fitting the functional forms.

DeleteFor example, the quantity theory of labor:

(NGDP/N0) = (L/L0)^k

CPI = (N0/L0) k (L/L0)^(k-1)

comes from the IE model. Fitting determines what N0, L0 and k are (e.g. k is about 4 for the US).

However, there is also

Numerical integration of the differential equation

A DSGE form derived from the differential equation

Simulations of the underlying degrees of freedom

Good post Jason

ReplyDeleteI think the best way to sum up what PK offers over the mainstream is that PK starts with banks as issuers of their own type of money and not intermediaries of savers and borrowers as mainstream seems to conceive them. There are are the concepts of "inside" and "outside" money, sometimes called horizontal or vertical money as well as the idea of different degrees of moneyless of various financial assets.

Understanding the role of reserves in the banking system is a huge issue. Listening to people describe the increased reserve levels we've seen since 2008 as "cash sitting idle in bank vaults waiting to be lent out" is getting painful.

I think you should look at PK a little closer. Monetary Realism is a great site to start ( I saw that they called you out a couple weeks ago!) Mike Sankowski and the prolific commenter, and author of a rare post , JKH would be prime resources to bounce your thoughts off of.

PK is the only school which integrates banking at the proper level in the economy I believe. Monetarists brag about not knowing anything about banking cuz its not necessary to their models and the rest treat reserves like they are gold.

Cheers, thanks.

DeleteI think JKH is where I got the reference/link to Godley-Lavoie above.

I'm not entirely sure what I am doing actually doesn't fall under the umbrella of Post Keynesianism. I say: agents aren't always rational, you can get stuck with low growth, financial "speculation" can trigger recessions, changes in base reserves don't cause inflation ...

I have no general problem with a lot of what has been said. And above, I list 3 pros (1 of which is that PK tends to be right about stuff) and 4 cons (2 of which I say are shared by all schools of economics).

I am planning on doing a post where I convert a stock-flow analysis into the language information equilibrium ... to compare and contrast the approaches.

"I am planning on doing a post where I convert a stock-flow analysis into the language information equilibrium ... to compare and contrast the approaches."

DeleteI'll be very interested in that!

It is rather ahistorical to argue Post Keynesians begin with a conclusion regarding desirability of government intervention when that conclusion was the result of empirical failure in classical economic theory during the Great Depression and subsequent empirical success of countercyclical stabilization policies emerging from Keynes work.

ReplyDeleteWhen I read this sort of thing it creates a strong impression of field-wide amnesia; as though nothing occurred prior to the rise of the New Classicals in the 1960s.

I was talking about present day Post Keynesianism, something that does not really exist until more recently (say, the 1970s).

DeleteBut even if that were the case, it does appear that even Keynes himself may have started with his conclusion and worked backwards ...

https://uneasymoney.com/2015/10/20/keynes-and-accounting-identities/

I think that the context of Keynes’s discussion of that identity [S = I] makes it clear that Keynes was not simply invoking the identity to prevent some logical slipup, as Pettis suggests, but was using it to deny the neoclassical Fisherian theory of interest which says that the rate of interest represents the intertemporal rate of substitution between present and future goods in consumption and the rate of transformation between present and future goods in production. Or, in less rigorous terminology, the rate of interest reflects the marginal rate of time preference and the marginal rate of productivity of capital. In its place, Keynes wanted to substitute a pure monetary or liquidity-preference theory of the rate of interest.

Keynes tried to show that the neoclassical theory could not possibly be right, inasmuch as, according to the theory, the equilibrium rate of interest is the rate that equilibrates the supply of with the demand for loanable funds.

Starting with the conclusion and working backwards doesn't necessarily make you wrong per se (I used this technique many times back in school) -- and Keynes was definitely right about contercyclical stabilization when inflation is low.

But accepting methodologies ex post based on policy outcomes isn't very scientific.

However, economics (heterodox and orthodox) isn't very scientific in general.

I'm not saying science is the only way to understand things either. Nor am I saying PK is pretending to be scientific. I am saying (in my opinion) it appears not to be scientific, and I prefer scientific approaches.

Jason,

DeleteThis is exactly the problem of not having sufficient historical geounding to understand the context of what one is reading. Keynes began with the assumption of validity of "classical" theory in his recommendations for post-war economic policy. This meant a return to the gold standard, austerity and limiting of trade deficits in balance of payments.

As the second post-war slump continued in the 1920s (according to the classical school the opposite should have happened) Keynes began to question the assumptions underlying those theories, later publishing 'The General Theory' as summation of his thinking. Keynes was responding to empirical failures and attempting to develop a new theory providing a better explanation. He was most certainly not out on some crackpot quest to prove a conclusion he came to out of nowhere.

P.S.

DeleteDrawing arbitrary lines through history is an unfortunately common mistake for non-historians who tend to assume linear relationships for the sake of clarity. Post-Keynesianism did not begin in the 1970s but developed in the work of Keynes' students as a continuation of his own.

Jason,

ReplyDeleteThoughtful as usual. I am not a card-carrying PKE, but I am a practitioner. Here are some key points you may have missed:

1. Identities are not behavioral relationships for sure, but most mainstream economics is very sloppy about this. They often work with real identities--which is nonsensical.

2. Macro identities also clearly expose fallacies of composition, eg. cutting wages increases profits in the aggregate.

3. Financial constraints and real constraints are not the same--eg. government debt is a burden on the future. You will see Nick Rowe concoct elaborate examples to show this is true, but a careful analysis will show that he assumes the result.

4. The economy is generally demand constrained.

5. Balance sheet positions matter (Minsky).

6. Growth is often constrained by balance of payments--Thirlwall and Kaldor. that is why export led strategy works, especially for EMs

7. Higher growth foster higher productivity (Kaldor-Verdoorn).

So much for now.

Hi Srini,

DeleteI am perfectly fine with everything you say here. Some minor quibbles:

1. I'd say the problem with identities is implicit modeling. And I'd agree that real (v. nominal) identities are nonsense.

5. Minsky is fine as a specific model of how recessions work, and may well lead to insight. But it is not currently known how recessions work. For my definition of "known", see here.

"And I'd agree that real (v. nominal) identities are nonsense."

DeleteCan you elaborate on this? I don't know what real identities are. I googled "real identities economics" and came up with this:

https://en.wikipedia.org/wiki/Balances_Mechanics

On the utility of accounting for economics

ReplyDeleteGiven

Y ≣ C + I + G + NX

it is true that

∂Y/∂G = 1

but that does not mean that

∆Y = ∆G ; "Keynesian stimulus".

It is also true that

∂I/∂G = −1

but that does not mean that

∆I = −∆G ; "Crowding out".

Given

S + T ≣ I + G + NX

it is true that

∂S/∂G = 1

but that does not mean that

∆S = ∆G ; "Ricardian equivalence".

Given

PQ = MV

or, equivalently,

lnP + lnQ = lnM + lnV

it is true that

∂lnP/∂lnM = 1

but that does not mean that

∆lnP = ∆lnM ; "Quantity theory of money".

On the surface, it appears as though economists sometimes reason from partial differentials, despite knowing about the fallacy of composition. (Sometimes they do, quite deliberately, but that is another matter, I think.) Accounting identities proved a check on the reasoning. Everyone agrees that they must be satisfied. It is therefore disquieting to hear economists disparage accounting identities.

Bill,

DeleteYou said

Given

Y ≣ C + I + G + NX

it is true that

∂Y/∂G = 1

This is not correct. In general, consumption and investment (and exports) may have some dependence on government spending, so the correct statement is:

∂Y/∂G = ∂C(G, ...)/∂G + ∂I(G, ...)/∂G + 1 + ∂NX(G, ...)/∂G

... in your comment above, you assume there is only explicit dependence, with no implicit dependence; this is incorrect in general.

"Everyone agrees that they must be satisfied. It is therefore disquieting to hear economists disparage accounting identities."

DeleteBut when you are trying to make causal inference from accounting identities, as some - a lot of - heterodox are doing, including sometimes Scott Sumner, you have a big misunderstanding problem.

Anonymous -- it is not so much misunderstanding as implicit modeling. And there is never any description/acknowledgement of what that implicit model is ...

DeleteWell, Jason, I was using the definition of partial differentiation that I learned as a kid, holding the other variables constant. A quick web search has not revealed any other definition.

DeleteYes, other independent variables.

Delete∂A/∂B = 0 if A is not a function of B

∂A(B)/∂B ≠ 0, generally.

If someone writes ∂f/∂x, is it always zero?

Is ∂Y/∂G = 0? No, because Y is a function of G. Y = Y(G, C, ...).

But unless we make the assumption that ∂C/∂G = 0, we must generally assume

Y = Y(G, C(G), I(G), NX(G)) = G + C(G) + I(G) + NX(G)

I do occasionally make mistakes, but this isn't one of them :)

Delete"I do occasionally make mistakes, but this isn't one of them"

DeleteI agree, it's pretty rare. Usually a mis-colored line in a plot or something. However, I never did figure out what went on here. Was I out to lunch on that one?

I don't think so -- I retracted the post because it may well have been wrong (not just the sign error, but the entire approach ... ).

DeleteI'd approach Cobb Douglas functions the way I do in the paper now -- with two independent markets.

DeleteAh, Ok. Thanks. You have a number of broken links leading to that page now. You can find them by typing in "Cobb" in your search box. I'd say at least 2 and maybe as many as 3 or 4 altogether.

DeleteThis particular one has the same expression, including the sign error.

DeleteI think I might leave it in there as a sign of my personal fallibility.

DeleteJason,

DeleteI am thinking both you and Bill are barking up the wrong tree.

Y = C + I + G + X does not express a functional relation so I can't see how the equation can be differentiated.

Let say you have four boxes labeled apples, oranges, bananas and pears.

A = weight of box of apples

O = weight of box of oranges

B = weight of box of oranges

P = weight of box of pears.

and

W = the total weight of all the boxes

So,

W = A + O + B + P

How can you then take the derivative of this expression?

Unless you can specify a functional relationship between any or all of the weights this cannot be done.

It's the same with the income accounting identity.

There is nothing you can tell about the functional relationships between any of the variables by looking at the equation.

I had a similar conversation with you last year about a paper John Cochrane wrote, in which I argued in my simplistic way, that the first equation presented by Cochrane was tautology and was not a valid way to begin his analysis. I don't think you were too pleased with my arguments.

The same thing is going on here. You are wont to take an identity and somehow make it into a functional relationship.

I am now wondering whether the seminal equation in the IE model is of a similar ilk, which if it is, I might begin to think about making the argument that your model is standing on shakey ground.

Henry

Henry,

DeleteThat form explicitly says the weight of the box of apples doesn't depend on the oranges.

And yes, you can build a model that way -- but it's not just an accounting identity. It is an accounting identity plus:

A is not a function of O, B and P

O is not a function of A, B and P

B is not a function of O, A and P

P is not a function of O, B and A

But among other things, that means that the Keynesian multiplier is just equal to 1 (instead of between 1 and 2 like many empirical studies say).

If an increase in G just increases Y through G

G → G + dG

Y → Y + α dG = Y + dG

Then the multiplier α = 1. But if

G → G + dG

Y → Y + α dG

with α not being 1, then consumption or investment must have some dependence on G so that

G → G + dG

C → C + x*dG

I → I + y*dG

And

Y → Y + α dG

With α = 1 + x + y.

The above is just a complete arm waving exercise.

DeleteYou can raise all the "ifs" you like - you haven't answered definitively the question, what causes changes in Y.

You cannot construct a meaningful functional model by just taking derivatives of the terms in the RHS. Before you can analyse changes in Y you must understand what causes changes in the terms in the RHS of the equation. You cannot discern this from the identity itself.

H.

Jason,

DeleteYour multiplier argument is a complete red herring.

H.

"A is not a function of O, B and P

DeleteO is not a function of A, B and P

B is not a function of O, A and P

P is not a function of O, B and A"

How can you say this from looking at the identity?

H.

Sorry to say this Jason, but all of the above demonstrates what happens when you let a mathematician loose on a subject. Functional relationships appear out of the ether. Where is the economic insight? There is none.

DeleteH.

Henry,

DeleteMy read (for what it's worth):

"A is not a function of O, B and P" ... etc, comes from this statement of yours:

"Let say you have four boxes labeled apples, oranges, bananas and pears. ..."

i.e. you made an pretty explicit model with that sentence. Thus A not depending on O, etc, follows. You can't get it directly from the identity since without your story about what the symbols represent, you have to assume:

(1) W = A(O,B,P) + O(A,B,P) + ... etc

If I were reading your fruit example in a word problem, I'd assume what Jason did in that case.

That said, if you didn't have your descriptive sentence, you'd have to assume something like my (1) and therefore you'd be correct.

As for Jason's example with Y, etc, I'm not seeing the problem. He's just doing the equivalent of assuming a function analogous to my (1).

Of course there could be more to your "word problem" that you left unsaid: like all the fruit in all the boxes represents the full harvest of all the fruit in the same finite area/water orchard, so one more apple tree means one less orange tree, etc... and then you could be right back with my equation (1).

Anyway, that's my read.

A is the weight of a box of apples, right?

DeleteIt has no oranges in it, right?

Then A does not depend on the weight of oranges.

So dA/dO = 0.

"Functional relationships appear out of the ether."

I know -- isn't it awesome? It's basic logic. If you say W = A + O and A and O are boxes of apples and oranges, you can logically deduce that dA/dO = 0 (that would make O a box of apples and oranges -- a contradiction) and therefore dW/dA = 1.

But the real economics comes in when because you can't say Y = C + G + I + NX is like a set of boxes. Each box has some apples and oranges (and pears, etc) in it. What you said about the boxes of fruit as an analogy is empirically false since Keynesian multipliers are not equal to 1. Consumption is not like a box of consumption widgets ... it has some government spending widgets in it (or at least consumption widgets made from government spending widgets).

Tom,

DeleteMy statement:

"Let say you have four boxes labeled apples, oranges, bananas and pears. ..."

is not a description of a model. A model expresses functional relationships between variables. I merely made a statement, "here is four boxes named thus". I made no explicit statement about how the contents of the boxes are related.

".....you have to assume:

(1) W = A(O,B,P) + O(A,B,P) + ... etc"

Not necessarily. You can propose such a relationship but not on the basis of my statement.

" He's just doing the equivalent of assuming a function analogous to my (1). "

Correct - assuming. On what grounds? There are no explicit grounds.

"Of course there could be more to your "word problem" that you left unsaid"

For sure, but you made that all up. That's the point. Same with Y = etc. All there is the identity. There is no information about and nothing that can be construed about the functional relationships between Y and variables and the between the variables themselves.

H.

Jason,

Delete"Then A does not depend on the weight of oranges."

That does not necessarily follow without more explicit information. This information cannot be gleaned from the identity itself. That's my point.

"you can logically deduce that dA/dO = 0"

No you can't - not without further information.

"(that would make O a box of apples and oranges -- a contradiction)"

I can't see the logical validity of that statement.

"But the real economics comes in when because you can't say Y = C + G + I + NX is like a set of boxes. "

But it is a set of boxes and that's ALL. It is this by DEFINITION.

"Each box has some apples and oranges (and pears, etc) in it. "

How can this be? This statement contradicts the definition of a box and its contents.

"What you said about the boxes of fruit as an analogy is empirically false since Keynesian multipliers are not equal to 1."

Again you introduce the red herring. We are not talking about empirically testing the identity. It doesn't need testing. It is true by definition.

"Consumption is not like a box of consumption widgets ... it has some government spending widgets in it (or at least consumption widgets made from government spending widgets"

Yes that is more or less correct in the real world of national income accounting. In national accounts, "Consumption" includes purchases by Gov. of non investment goods. They are all consumption goods and they are accounted for under "Consumption". That's the way national income accounts are constructed. Here, we are talking about a theoretical economic identity, we are not dealing with national accounting practice.

Henry, yes, I know I made all that up. That was my point. And sure, you weren't specific about every detail in your description. I get it. It's just that it suggests there's not something more going on behind the scenes (as in the case I made up). If I saw this as a word problem:

Delete"Two cars approach each other. One is going X mph and the other Y mph..."

w/o any other info, I'd assume they were headed directly for each other. That their range rate was -(X+Y). Of course it COULD be that they aren't going directly at each other (but are nonetheless approaching each other), etc. That's sometimes the basis of good puzzles BTW.

Have you heard this one? (and can you solve it)?

A young childless man takes a trip to visit the pyramids. Years later he takes his son to visit them.

The man made his solo trip to the pyramids in 1983, but he went with his son in 1959. How is this possible?

"That does not necessarily follow without more explicit information"

DeleteWhat pray tell is that more explicit information? It's that an apple is not an orange. So yes, if an apple is an orange, then you can't proceed as I did. But by calling them apples and oranges, I assumed (silly me) that apples are not oranges.

So sorry. I guess pears are oranges too? Are pears apples? Is weight fruit? Is investment a box? The economy is the weight of a pear? What is is? Is is not?

This comment has been removed by the author.

Delete"yes, I know I made all that up. That was my point. And sure, you weren't specific about every detail in your description. I get it. It's just that it suggests there's not something more going on behind the scenes (as in the case I made up)."

DeleteWhen an economist defines the income flow equation as Y = ........etc. then that's it. It's a definition. That's all it is. No conclusions can be drawn regarding the factors that cause changes in the variables nominated.

"What pray tell is that more explicit information?"

DeleteYou have to look at each variable and formulate hypotheses about what causes changes in them.

For instance, Keynes, in developing his theory of effective demand hypothesised:

C = aY +b

It was an hypothesis. He made an argument in support of it. He left it to others to test.

"C = aY + b"

DeleteThat was my #@$%ing point!!!!!

C = a Y(G) + b

so dC/dG = a dY/dG is not zero.

... i give up ...

Jason,

DeleteYou may have got to the some place but you got there via a different line of reasoning.

You began with the identity.

Keynes postulated a functional relationship ab initio.

Is there not a difference?

I don't understand the difference between "postulating a functional relationship" and saying we can't assume there isn't a functional relationship.

Delete??????

Saying X is the still same as NOT(NOT(X)) right? Someone didn't go and change the rules of logic on me again ... did they?

Henry, I just meant in regard to your fruit example.

Delete"I don't understand the difference between "postulating a functional relationship" and saying we can't assume there isn't a functional relationship."

DeleteBut you use as your functional relationship an identity.

Is that not correct?

The economy is a complex system. The basic assumption is that everything is interdependent.

ReplyDeleteJason: "But unless we make the assumption that ∂C/∂G = 0, we must generally assume

Y = Y(G, C(G), I(G), NX(G)) = G + C(G) + I(G) + NX(G)"

In that case, everything is a function of G, and we are not talking about partial differentiation, are we?

In any event, the point of my comment lies here:

"that does not mean that

∆Y = ∆G ; "Keynesian stimulus". . . .

"that does not mean that

∆I = −∆G ; "Crowding out". . . .

" that does not mean that

∆S = ∆G ; "Ricardian equivalence". . . .

"that does not mean that

∆lnP = ∆lnM ; "Quantity theory of money". . . .

"Accounting identities provide a check on the reasoning." :)

"In that case, everything is a function of G, and we are not talking about partial differentiation, are we?"

DeletePartial differentiation isn't a constraint on the function. We don't know the dependence of C on G, so we can't assume it is zero.

The rest of your comment makes implicit assumptions about the models ...

Accounting identities can provide a check on your math, but are basically useless for reasoning ... Unless you make implicit assumptions along with those accounting identities.

DeleteSee also my comment directly above yours. Assuming C and I have no dependence on G means the Keynesian multiplier is 1 (and not between 1 and 2 as many empirical studies say).

DeleteJason: "Partial differentiation isn't a constraint on the function. We don't know the dependence of C on G, so we can't assume it is zero.

Delete"The rest of your comment makes implicit assumptions about the models ..."

Yes, because I was trying to come up with something similar to other people's ideas. I wasn't trying to model my own. As I said, my belief is in interdependence.

Bill, above you introduce this symbol: ≣

ReplyDeleteI'm used to three bars meaning "defined as." I just read your symbol as "defined as" but does the 4th bar impart any other meaning?

He probably meant triple bar there.

DeleteJason, you may have noticed that Nick Rowe has a post up discussing implicit modeling with accounting identities:

ReplyDeleteThe problem is this: If Y = X + Z, and we ask "does X count towards Y?", we are making an implicit assumption about whether or not Z stays the same. The number of my Kids equals the number of my Sons plus the number of my Daughters. K=S+D is an accounting identity. Does "if I have one more son" mean "if I have one more son and the same number of daughters" or "if I have one more son instead of having a daughter"?

Nick's son and daughter model makes several implicit assumptions that aren't even relevant to the implicit assumptions in the questions.

DeleteE.g. dS/dD = 0 ... does the number of daughters influence the number of sons? In econ, government spending can influence the amount of consumption -- making the multiplier greater than 1.

Jason, taking another look at Noah's "Occult" post today, I noticed this comment from JW Mason about a guy named Ellis Scharfenaker, a new hire at UMKC:

ReplyDelete"Ellis Scharfenaker, wrote a dissertation that "combines novel approaches from information theory, statistical mechanics, and Bayesian reasoning..."

His name didn't come up in your search box. Have you heard of him?

Nope.

DeleteAlso work is totally different. He seems to be using utility as energy and there is a decision temperature. He seems to be in the vein of Duncan Foley.

Just because they mention information theory, Shannon or stat mech doesn't mean it's in any way related.

A good way to realize that is you can mention all of those things and not be talking about economics, but rather about black hole thermodynamics.