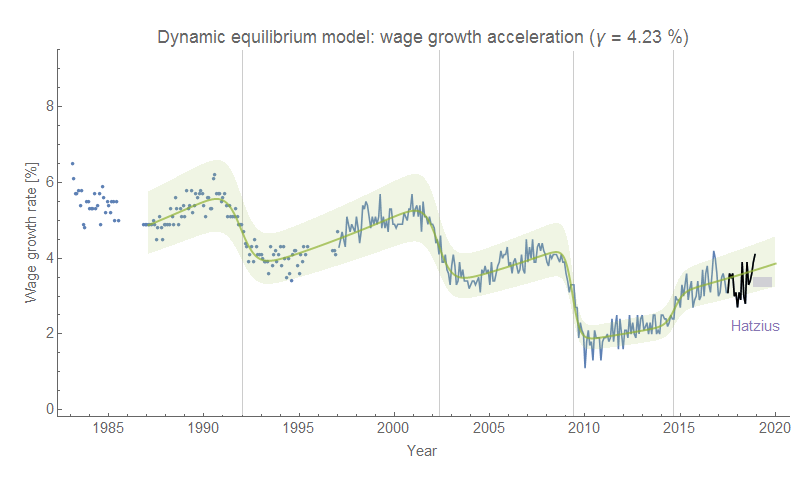

I haven't compared the wage growth forecast to the Atlanta Fed's wage growth tracker data in awhile (last time was here). The recent data remains consistent with the forecast accelerating growth (increase in the growth rate):

(The "Hatzius" marking is from this post comparing the highly paid Goldman Sach's chief economist Jan Hatzius with the dynamic information equilibrium models.)

This model comparing various labor market measures estimates that wage growth lags changes in JOLTS hires by 11 months, and changes in the unemployment rate by 6 months — that is to say a recession (defined as a spike in unemployment) precedes a drop in wage growth. An intuitive interpretation is that recessions "cut-off" wage growth.

What is also interesting is that wage growth appears to experience a negative shock when it reaches NGDP growth, and the latest data is beginning to rise above the NGDP model:

There is an intuitive explanation behind this effect: if average wages are growing faster than average growth, eventually it should start to degrade firm profitability. Over the next year we should get a good test of the usefulness of the dynamic information equilibrium framework and this hypothesis.