Scott Sumner linked to Marcus Nunes about Australia avoiding the Great Recession today which gave me as good a reason as any to do this for that country. It is an interesting case because -- at least for the interest rates -- it doesn't work as well. Anyway, let's start with the NGDP (red) and MB (blue) in billions of Australian dollars:

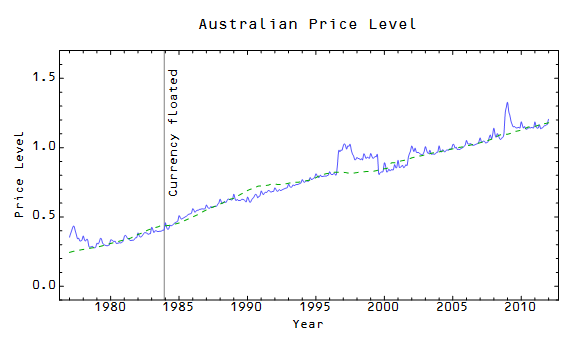

We can immediately do the fit to the price level (CPI less food, energy is in green and the model is in blue) and see that it is quite excellent:

However the interest rate model only works after the 1990s (3-month rate in green, model in blue):

I originally thought it might have something to do Australia floating its currency at the end of 1983 (hence the demarcation), but that doesn't seem to really account for it. I'm not sure what is responsible for the deviation. The EU shows some deviation from the model as well, but it doesn't have quite the same magnitude as we see here.

The amazing economic feat Australia has accomplished is that it hasn't had a recession since the 1990s that is attributed to the RBA. However the price level parameters put Australia somewhat farther away from the information trap: it has a very low normalized monetary base like the UK, but additionally has a much lower information transfer index like the US. I've added Australia to the graph here:

Basically Australia was much farther from the information trap criterion (black dotted curve) and so its monetary base injection didn't push the country into the information trap (liquidity trap). However, we can see that Australia (gray) has a similar information transfer index to the US (blue), so it drives home the point that the information transfer index is not the only thing to consider:

No comments:

Post a Comment

Comments are welcome. Please see the Moderation and comment policy.

Also, try to avoid the use of dollar signs as they interfere with my setup of mathjax. I left it set up that way because I think this is funny for an economics blog. You can use € or £ instead.

Note: Only a member of this blog may post a comment.